At the Uncertainty Project, we explore models and techniques for managing uncertainty, decision making, and strategy. Every week we package up our learnings and share them with the 1,500+ leaders like you that read this newsletter!

In case you missed it, last week we kicked off 2024 with a post on Organizational Sensemaking - a look at how organizations construct reality, apply meaning, and make decisions

Let’s make ‘Portfolio’ a verb

Portfolio (noun)

A large, thin, flat case for loose sheets of paper such as drawings or maps.

a set of pieces of creative work collected by someone to display their skills, especially to a potential employer.

a varied set of photographs of a model or actor intended to be shown to a potential employer.

A range of investments held by a person or organization.

a range of products or services offered by an organization, especially when considered as a business asset.

The position and duties of a minister of state or a member of a cabinet.

So the dictionary tells us that the word ‘portfolio’ is a noun. A thing that we create. But the active management of this thing is where the magic happens. For that reason, we propose that we should use ‘portfolio’ more as a verb, to emphasize the action.

As in, “I have the responsibility to ‘portfolio’ that set of things…”

But first some background: Why do we form portfolios of things?

We use portfolios to help us “do more with less”, in the presence of uncertainty.

To see and manage a set of items as a whole

To balance risk across the set

To consolidate and rationalize the items

To optimize the value of the whole

When you “portfolio” a collection of things, you shift the game from optimizing individual things, to optimizing the whole. To see it as a coherent set of things to balance and manage as one.

These things can range from projects, to businesses, to IT assets, to designs, to offers, to suppliers, to partners, to people. All carry variable risks, and expected returns. In the presence of uncertainty, we use portfolios to help manage this risk.

“An easy way to think about this.. is that anything you can consolidate or rationalize is a portfolio.”

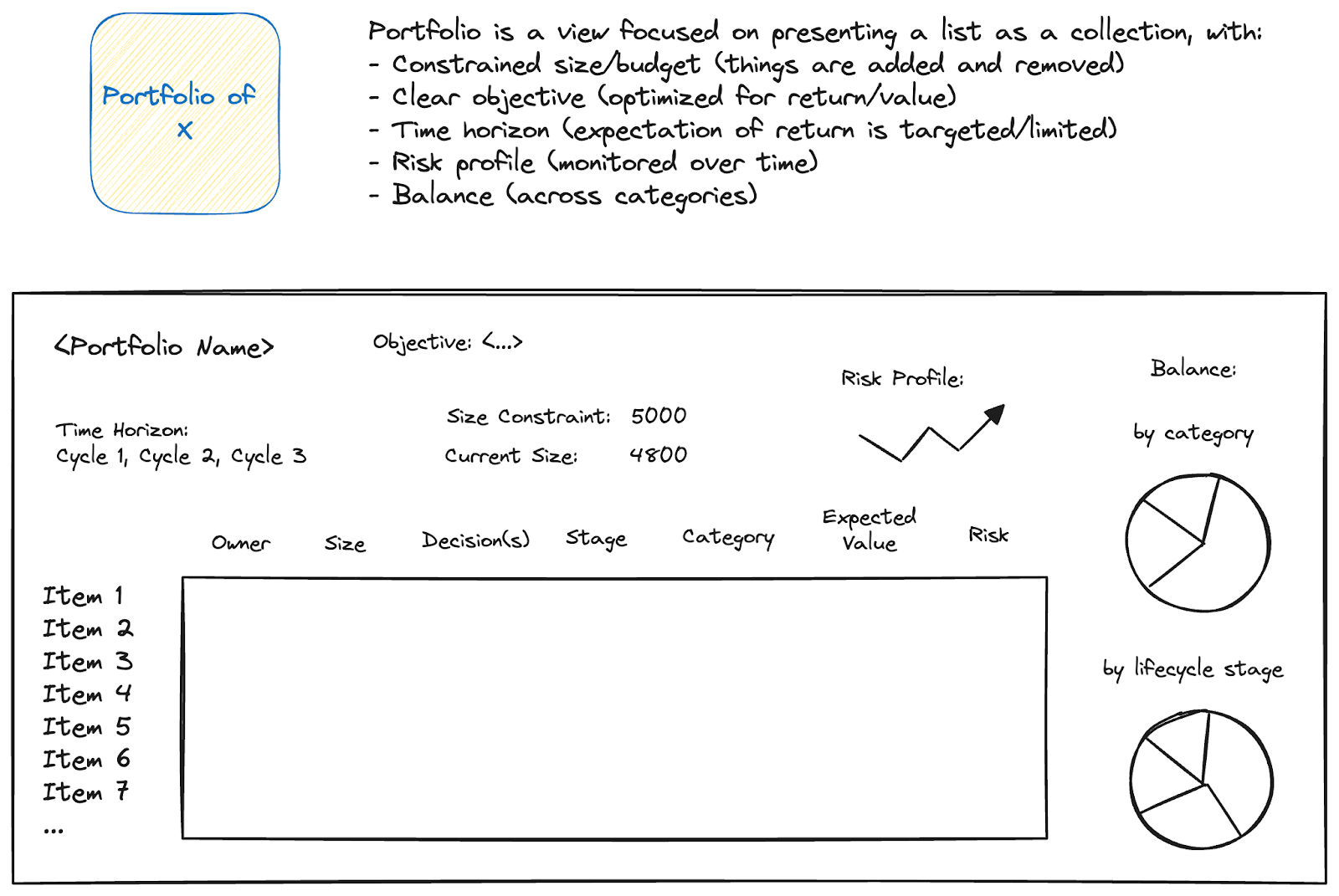

Portfolios share some characteristics:

They are a collection of things with different risk levels. That is, some things will perform better than others, and we can’t predict which ones (at least not very well).

The time horizon of the collection is fixed. Since we will be assessing risk and value, the time dimension is relevant. We might be looking for short-term gains, or pursuing long-term returns. A specific portfolio should be framed to make this clear.

The size (or budget) of the collection is bounded. We are always considering whether something that is not in the collection (right now) might be better than something currently in the collection.

The collection is actively managed. The assessment of risk is continuous, so the management of the portfolio is continuous as well.

The collection is assessed by value (or return), and the risks that drive current understanding of expected value. Assessments of value can change. And risks will change, too.

There will be trade-offs when building a collection, and these trade-offs frame the assessments of value. They help keep a portfolio “balanced” in some way. This is an attribute of the collection, given a specific position on the desired balance between risk and return..

So there is a lot of activity in that list! Instead of a passive collection, a portfolio must be actively “portfolio-ed”.

Possible visualization of a generic portfolio - full screen

Here we explore some common mechanics of “portfolio-ing” that can be applied universally, to collections of different kinds of things.

Some steps to “portfolio” a list of stuff: (assumes you already have a bunch of stuff)

Clarify the objectives (and/or scope boundaries)

Set a size/capacity limit

Define a lifecycle for the portfolio items

Define a way to assess risk that includes % and impact

Define balance, in multiple dimensions

Define a cadence for re-evaluating the composition of the portfolio

Objectives

Portfolios are collections of things that represent assets or investments of some kind. These things are expected to deliver some value or return in the future, but there is much uncertainty when dealing with the future. So we search for things that might deliver on our objectives and pool them together, to hedge our bets. Note how the decision to create a portfolio should be an explicit statement that acknowledges the challenges of uncertainty!

A portfolio manager must be clear on the purpose of the portfolio, and what mission it serves. While this purpose should be relatively static, there could be times when a dramatic shift in strategy could force a revisit to the intent and objectives of an existing portfolio. Strategic shifts should drive a recalibration and fresh rationalization of a portfolio.

Size

Portfolios have a constraint on their size. This is usually a budget of some kind, such that the sum of the cost of the assets in the portfolio will not exceed the constraint. The size can change over time, but the constraint is still a factor.

So the portfolio manager actively monitors the set of things in the collection and asks, “Given the size constraint, should I consider adding this new thing, and removing this other thing from the portfolio?”

Lifecycle

The things in the portfolio will most likely have some lifecycle to track. Whether we are collecting entire businesses, IT assets, strategic investments, or products, these things generally move from cradle to grave in some way. Understanding where they sit in their lifecycle will be critical to optimizing the whole.

A portfolio manager must continuously monitor the things in the collection, to assess where each item currently sits in their individual lifecycle, since this can (and will) drive the risk and expected value. This is often a judgment call, and worthy of collaborative dialog.

Risk

A portfolio is primarily a risk management tool. Its strength lies in the way it helps us navigate uncertainty. The owner of the portfolio will need to be clear on their appetite or tolerance for risk up front, since the selection of items should reflect that appetite. This is as true in a financial portfolio as it is in a product portfolio; the desired level of risk should be transparent at all times.

A portfolio manager will assess the risk levels of the things in the collection, as they evolve, and as the context they live in evolves. This risk to value (or return) will be influenced by many, many things, and monitoring all this is the biggest job of the portfolio manager.

“Never ask anyone for their opinion, forecast, or recommendation. Just ask them what they have—or don’t have—in their portfolio.”

Balance

The magic of a portfolio lies in its ability to offset risks in one individual thing with the (different) risks of another thing in the collection. Sometimes this balance is found in a set of similar (or even redundant) things that will react differently to the future changes in context. In this situation, you build a collection of options instead of trying to pick the winner. Other times, you set expectations for balancing the portfolio across a variety of categories or types of things, with an intent to achieve different flavors of returns from the collection.

A portfolio manager defines this desired balance before building a portfolio. This will vary with the kind of portfolio. The financial portfolio is a well-known example, where a balance between stocks, bonds, and cash, and/or large-cap, small-cap, and international stocks help define the goals of the portfolio itself. For any portfolio, a similar discussion of balance can be found.

This is arguably the most important part of “portfolio-ing”. A portfolio gets its super-powers from its ability to diversify, and through that, manage risk and uncertainty. Putting all your eggs in one basket is gambling. Diversifying across risk profiles… now that’s “portfolio-ing”.

Cadence

By now, you should hopefully see that actively managing a portfolio takes some ongoing effort. But how much? How frequently (realistically) should we review the composition of (and the risk profile of) the collection? Wait too long to rebalance or adjust, and the portfolio will underperform. Monitor changes too frequently, and you’ll likely overreact (and go crazy).

Portfolio managers can pick a cadence (e.g. quarterly, or every 6 months) to share and update on the composition and performance of their portfolio, with their stakeholders. This forcing function will also encourage the manager to consider making appropriate changes, driven by changes in perceived risk.

At the end of the day, a portfolio is a tool to help manage change. But while the portfolio can help frame decisions, it won’t point the way.

“It goes without saying that the most critical aspect in portfolio analysis is a decision on what changes, if any, are necessary. Unfortunately, most of the standard portfolio models do not offer explicit guidelines for establishing an optimal portfolio. For example, classifying certain products as dogs, problem children, cash cows, and stars does not help determine their optimal mix.” - “Designing Business and Product Portfolios”, Yoram (Jerry) Wind and Vijay Mahajan - Harvard Business Review.

With true investment portfolios, optimization can get very technical and mathematical. [We introduced some Modern Portfolio Theory in an earlier post.]

But some of the most successful have found success by keeping it simple.

“The greater the potential for reward in the value portfolio, the less risk there is.”

“Beta and modern portfolio theory and the like - none of it makes any sense to me.”

We believe that for portfolios of products, projects, IT assets, and strategic investments, the challenge is less technical, and more social. Collaborating to assess risk, monitor progress, understand changes in the environment, and exposing uncertainty is difficult. When many stakeholders are involved (as is usually the case), the need for transparency drives a significant communication challenge.

“The most important asset you need to protect in order to manage the demands of a job or an investment portfolio is your production of energy. And, just like with money, if you do a great job managing your energy, you'll get a great return.”

Solving this people problem by creating practices that bring the right people, to the right dialog, at the right time is a better way to get started than fine-tuning those formulas in your Excel sheet. Get started by socializing the concept of “portfolio-ing”. Talk about what effective “portfolio-ing” needs:

How much time should be devoted each quarter?

How much effort should be spent monitoring the things?

Who should be involved in the monitoring efforts? How?

Who should be involved in the periodic reviews? How?

Where should meaningful dialog of risk and uncertainty happen?

If you’re lucky, then your portfolios will be collections of static things that quietly crank out returns. But in this modern world, it’s more likely that, for a portfolio:

The things in your collection are changing a lot

The environment around them is changing a lot

People’s expectations are changing a lot

And maybe… your purpose is even changing

So like other words that effectively serve as both nouns and verbs (see: alert, estimate, signal, change, study, practice, progress), let’s give the word “portfolio” an upgrade. To a verb.

Maybe that can help us to get more serious about “portfolio-ing”.

How was this week's post?

If you’re out there and want to contribute a post (on topics around strategy, decision making, and dealing with uncertainty) - we’d love to chat! Feel free to reply to this email!

And again, we’ve set up a series of 5 live sessions to cover topics around Decision Architecture. It’s free and exclusive to Uncertainty Project subscribers, but we will have a limited number of spots (just to make sure we can facilitate/manage actual discussion). Sign up for the waitlist if you’re interested!